How to Make a Budget with the 50/30/20 Rule: A 15-Minute Guide

Making a budget takes three steps: figure out your net income, split it into needs, wants, and savings, and give every category a fixed monthly amount. The 50/30/20 rule hands you a ready-made split — and this guide works through it with a $3,000 net income example.

What is a budget — and why do you need one?

A budget is a plan that gives every dollar of your income a job before the month starts: this much for rent, this much for groceries, this much for fun, this much into savings. That's the difference from plain expense tracking: a tracker shows you afterwards where the money went — a budget decides beforehand where it should go.

Without a budget, most months follow the same script: the account feels full at the start, the second half turns into mental math, and nothing is left to save at the end. A monthly budget flips that around — savings and fixed costs are allocated first, and whatever is set aside for wants you can spend guilt-free.

The 50/30/20 rule explained

The 50/30/20 rule is a rule of thumb that splits your net income into three buckets:

- 50% needs and fixed costs: Everything you need to live — rent, utilities, groceries, insurance, transport, phone plan.

- 30% wants: Everything that makes life enjoyable but is technically optional — restaurants, streaming, hobbies, shopping, travel.

- 20% savings and debt payoff: Emergency fund, savings goals, investing — or paying down debt, because every dollar of debt you clear is money saved.

The appeal of the rule: you don't have to reason through 30 categories one by one — you make a single top-level decision. And it deliberately reserves 30% for wants, because a budget built purely on sacrifice is one nobody sticks to.

Worked example: a monthly budget on $3,000 net

- $1,500 needs: e.g. $950 rent and utilities, $350 groceries, $120 insurance, $80 transport and phone.

- $900 wants: e.g. $250 eating out, $50 streaming and subscriptions, $250 hobbies and shopping, $350 vacation fund.

- $600 savings: e.g. $250 into your emergency fund, $350 into savings goals or debt payoff.

Important: 50/30/20 is a starting point, not a law. If rent in an expensive city already eats 45% on its own, your split becomes 60/25/15 for a while — what matters is that you have a deliberate allocation at all, and that your savings rate never drops to zero.

How to plan your monthly budget, step by step

1. Determine your net income (2 minutes)

Use the money that actually lands in your account. If your income varies, work with a cautious average of the last few months — better to estimate low than high.

2. List your fixed costs (5 minutes)

Go through the last two or three months of your account and write down every recurring charge: rent, utilities, insurance, subscriptions. Divide yearly bills like car insurance by twelve so they can't ambush you in the month they're due.

3. Fill the three buckets (5 minutes)

Apply 50/30/20 to your net income and distribute the buckets across concrete categories with fixed amounts. Eight to twelve categories are plenty — an overly fine split makes budgeting a chore.

4. Track against it during the month (ongoing)

A budget only works if you hold your real spending against it. Log every expense in its category and glance at what's still available before bigger purchases — that's exactly the idea behind envelope budgeting.

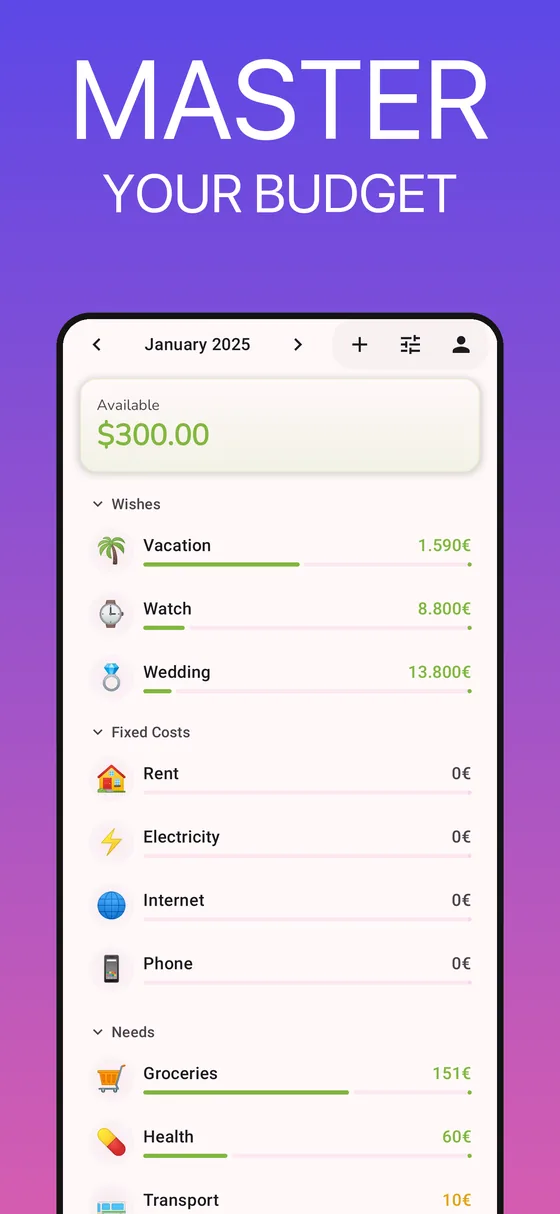

How to do it in GetALife

GetALife is built around exactly this budgeting principle:

- Category groups that match the rule: On the budget screen you organize categories into groups like needs, wants, and fixed costs — a one-to-one mapping of the 50/30/20 split.

- Limits per category: Each category gets its monthly amount as a limit — $350 for groceries, $250 for eating out.

- The "Available" amount: Every category shows how much is left this month. Before an impulse buy, one glance replaces mental math.

- Analytics dashboard: Trends and category breakdowns show you after a few weeks whether your split was realistic — and where to adjust.

- Frictionless logging: Entering a transaction takes seconds; with Premium you can log by AI voice input ("groceries 47 dollars") or automatically via bank sync. Budget tracking itself is free.

Common budgeting mistakes — and how to avoid them

- Starting too ambitious: A first budget with a 40% savings rate collapses in month two. Start realistic and raise the savings rate gradually.

- Setting wants to zero: A budget with no fun bucket is a diet with no cheat day — it fails on psychology, not math.

- Forgetting irregular costs: Gifts, car repairs, annual fees. Give them their own category with a monthly set-aside.

- Making a budget but never tracking: The plan alone changes nothing. Only the comparison with your real spending turns a spreadsheet into a tool.

Conclusion

With the 50/30/20 rule, making a budget takes less than fifteen minutes: determine your net income, calculate the three buckets, assign categories with fixed amounts. The split doesn't have to be perfect — it just has to exist and be checked against your real spending. Routine does the rest.

Make your budget today

GetALife is free, works offline, and turns your monthly budget into a game you actually want to win.