Emergency Fund Calculator: How Much Do You Really Need?

The rule of thumb: keep three to six months of expenses as your emergency fund. If you spend $2,300 a month, that means $6,900 to $13,800. Where you land in that range depends on your job security, your family situation, and whether you own your home — here is the full calculation.

What is an emergency fund — and what is it for?

An emergency fund is a cash reserve for genuine emergencies: the washing machine dies, the car needs a new clutch, the job suddenly disappears. It is not a vacation fund and not a savings goal for wants — it exists purely so that one unexpected hit does not push you into overdraft or debt.

That is why it comes first in any savings plan: before you invest or save for bigger goals, the emergency fund makes sure a single emergency cannot wreck your entire financial setup.

The rule of thumb: 3 to 6 months of expenses

The common recommendation is three to six months of expenses. Important: this is a rule of thumb, not a law of nature. Where you should land within that range depends mainly on three factors:

- Job security: Permanent contract in an in-demand field? Three months is usually enough. Self-employed, on a fixed-term contract, or with fluctuating income? Aim for six months or more.

- Family: If kids or a partner depend on you, you need more buffer than a single household — more people simply means more emergencies can happen at once.

- Homeownership: Owning your home means the furnace, the roof, and the plumbing are your problem. Homeowners should plan at the upper end of the range.

One more thing matters: the rule counts monthly expenses, not monthly income. If you earn $3,600 but spend $2,300, you only need to cover the $2,300.

How to calculate your emergency fund — with an example

The calculation takes just two steps:

1. Work out your monthly expenses

Add up everything that actually leaves your account each month: rent, utilities, groceries, insurance, transport, subscriptions. Most people underestimate this number — a look at a real expense tracker showing your actual spending over the last few months is far more reliable than guessing.

2. Multiply by your factor

Pick a number between 3 and 6 based on the factors above, then multiply:

- Example: Monthly expenses of $2,300, permanent job, one kid, renting → factor 4.

- Calculation: $2,300 × 4 = $9,200 emergency fund.

That number is your target. It does not have to be reached by tomorrow — but it should be concrete, because "building a reserve someday" is a resolution that never ends.

Where should you keep the money?

Your emergency fund has to do two things: be available at any time and stay out of accidental spending. A separate savings account works well for both — kept apart from your checking account. The separation is the real trick: money you do not see when paying is money you do not spend on impulse.

Brokerage accounts and fixed-term deposits are the wrong place: stocks can be down exactly when you need the cash, and locked deposits are unavailable in an emergency. The emergency fund is not there to earn — it is there to be there.

How to save it up

The most reliable method is automation: set up a standing transfer that moves a fixed amount to your savings account right after payday. That way you save before you can spend — instead of saving whatever happens to be left. How much per month is realistic? Your budget will tell you: even $100 to $200 a month gets you to the example target within two to three years — and every intermediate milestone already protects you.

How to do it in GetALife

GetALife takes care of the two hardest parts: an honest starting number and staying on track.

- Real monthly expenses instead of guesses: The expense tracker shows what you actually spent over the past months — the reliable base for your emergency fund calculation. Log expenses by hand, by AI voice input ("groceries 47 dollars"), or automatically via bank sync (both Premium — budget tracking itself is free).

- A savings goal with visible progress: Create "Emergency fund" as a savings goal with your target amount and watch the progress bar fill with every deposit.

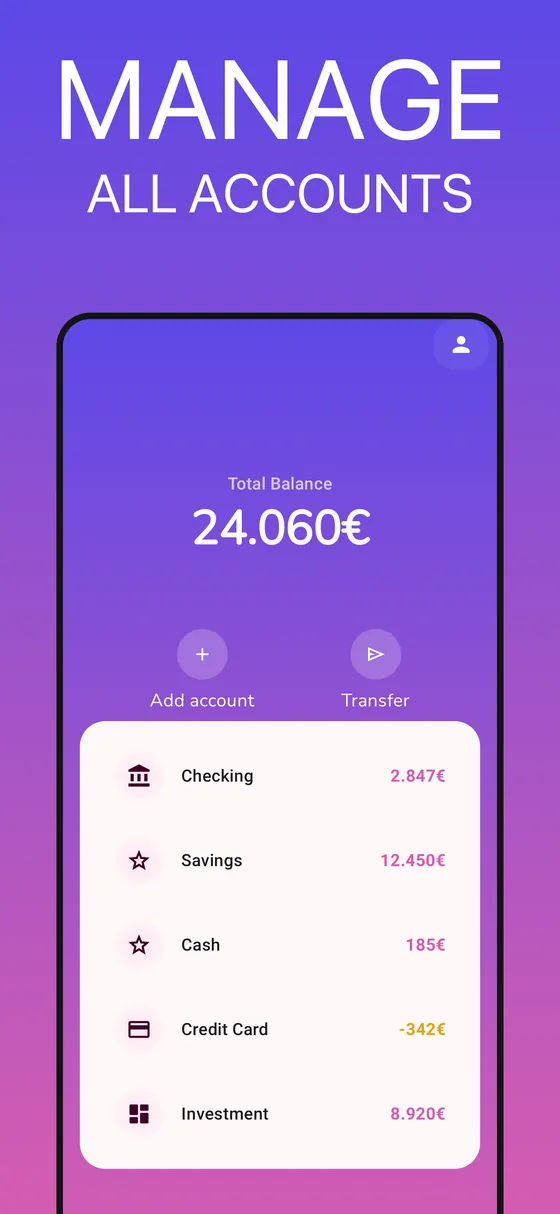

- All accounts in one view: Savings, checking, cash, and credit card sit side by side in the account overview — your emergency fund stays cleanly separated yet always visible.

- Runway as a sanity check: Your financial runway shows how many months your money lasts without income — the perfect cross-check that your fund really covers 3 to 6 months.

Common emergency fund mistakes — and how to avoid them

- Keeping it in your checking account: Money sitting between rent and grocery runs melts away. Separate account, clear boundary.

- Calculating with income: The rule of thumb means expenses. Multiplying your salary sets an unnecessarily high target — and makes you give up sooner.

- Investing the emergency fund: Returns are the job of your other savings goals. The emergency fund needs availability, not market upside.

- Not refilling after an emergency: Spending it is exactly what it is for — but afterwards, the standing transfer goes back on until the target is rebuilt.

Bottom line

Calculating your emergency fund takes five minutes: find your real monthly expenses, multiply by a factor between 3 and 6, done. The real work is saving it up — and that becomes easy once you automate it and can see your progress. A concrete target number plus an automatic transfer beats every good intention.

Build your emergency fund with GetALife

GetALife shows your real monthly expenses, tracks your savings goal with visual progress — and your runway tells you how long your cushion actually lasts.