Net Worth Tracker: The One Number That Shows Your Real Progress

Your net worth is everything you own minus everything you owe: assets minus liabilities. This single number is the most honest indicator of your financial progress — far more honest than your bank balance. Here is how to calculate it, with a worked example, and how to track it over time.

What is net worth?

The formula is simple: net worth = assets − liabilities. On one side sits everything you own that has a monetary value. On the other side, everything you still have to pay back. The difference is what is truly yours — and yes, your net worth can be negative, for example right after graduation or after buying a home. That is no reason to panic; it is simply the starting point you improve from.

What counts — and what does not?

Assets include:

- Checking, savings, and money market accounts

- Brokerage accounts: ETFs, stocks, funds (at current market value)

- Cash

- Real estate (valued conservatively at a realistic sale price, not a wishful one)

Liabilities include:

- Mortgage and car loans (remaining balance)

- Outstanding credit card balances and overdrafts

- Buy-now-pay-later installments

- Student loans

Everyday possessions like your car, furniture, or electronics are fine to leave out: their resale value is uncertain, and they dilute the number more than they help it. Consistency beats completeness — what matters is that you calculate by the same rules every month.

Worked example: net worth in three steps

Take someone in their early thirties with a job and a monthly ETF plan:

- Step 1 — add up assets: Checking $1,400 + savings $7,000 + ETF portfolio $10,500 + cash $300 = $19,200

- Step 2 — add up liabilities: Car loan balance $5,000 + credit card balance $900 + student loans $6,800 = $12,700

- Step 3 — take the difference: $19,200 − $12,700 = $6,500 net worth

The bank balance alone ($1,400) would have painted a completely wrong picture — in both directions: it ignores the portfolio just as much as the debt.

Why this number beats your bank balance

Your bank balance is a snapshot that constantly lies: it looks great right after payday and miserable right after rent — and it says nothing about your investments or your loans. Net worth, on the other hand, is an honest progress indicator: it only goes up when you actually move forward.

It is especially motivating when paying off debt: on your checking account, every loan payment just looks like money disappearing — but in your net worth, every single payment visibly pushes the number up. That effect keeps you going where pure willpower gives up. And if you are building an emergency fund or investing, both show up in one combined metric.

How often should you measure it?

Once a month is plenty — for example on the first of each month. Checking daily adds nothing: market prices fluctuate, and the noise hides the trend. What counts is the direction over months and years. A fixed monthly date turns it into a five-minute ritual — provided your accounts are tracked in one place, for instance in an expense tracker app.

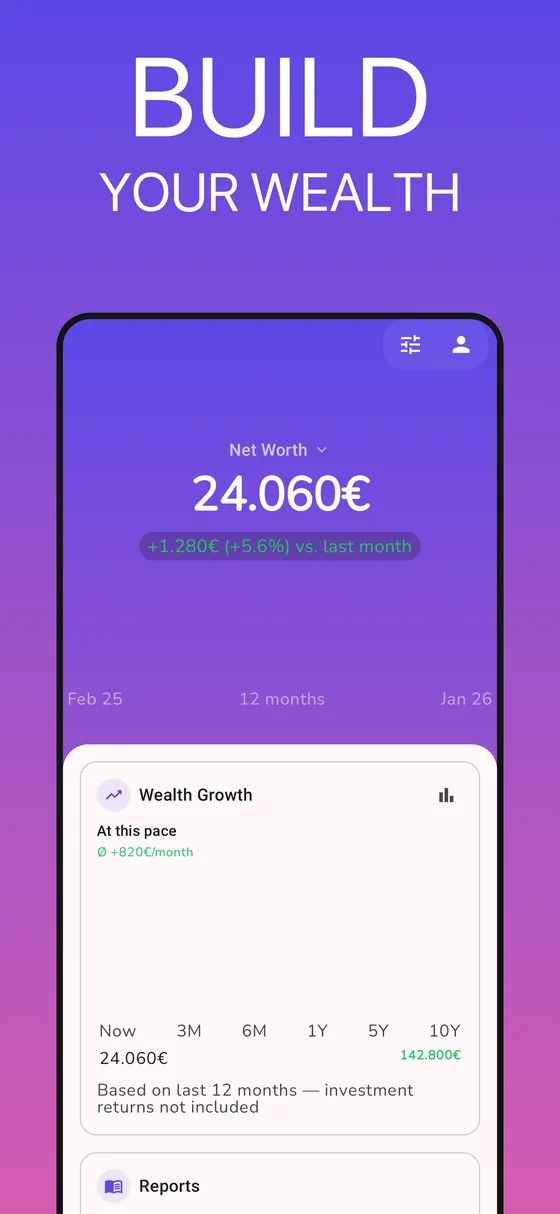

How to do it in GetALife

GetALife has a net worth calculator built in — no spreadsheet required:

- Add accounts and debts: Checking, savings, cash, ETF portfolio, and credit card all live as accounts. The app automatically nets assets against liabilities to show your net worth.

- A trend line instead of a snapshot: You see your net worth as a curve over the last 12 months — the trend is visible at a glance.

- Projection into the future: Based on your savings rate, GetALife projects where your wealth is heading if you keep going like this.

- Up-to-date numbers without busywork: Log transactions by hand, by AI voice input, or automatically via bank sync (voice input and bank sync are Premium — budget and net worth tracking itself is free).

- A liquidity cross-check: Your financial runway additionally shows how many months your money lasts without income — wealth and availability are two different questions, after all.

Common net worth mistakes — and how to avoid them

- Leaving out debt: Without liabilities, the number is self-deception. Overdrafts and installment purchases belong in there too.

- Overvaluing your home: Wishful prices inflate your assets. Value conservatively — and do not forget the remaining mortgage balance.

- Checking daily: Market swings are noise. Measure monthly, watch the trend.

- Comparing yourself to others: The only comparison that matters is your own number from last month.

Bottom line

Calculating your net worth means: everything you own minus everything you owe — a five-minute exercise once your accounts are tracked in one place. The real payoff comes from repetition: track the number monthly and you see genuine progress instead of bank balance snapshots — and you stay motivated, whether you are saving up or paying down debt.

Track your net worth with GetALife

GetALife nets your accounts and debts automatically, shows the 12-month history, and projects where your wealth is heading.